Part of The Kodgeti Ecosystem: Joyful Faith Thrives | Kodgeti Group | Intentional Gifting

Unlocking Wealth: The 5-Step Blueprint Using Insurance to Buy Real Estate

Understanding the Double Play Strategy

The innovative strategy of utilizing insurance as a means to purchase real estate is often termed the "double play" or "infinite banking." This approach is primarily favored by high-net-worth investors who seek to optimize the flow of their capital. By leveraging a specialized life insurance policy, investors can utilize their funds to work in two different arenas simultaneously—real estate investment and life insurance accumulation.

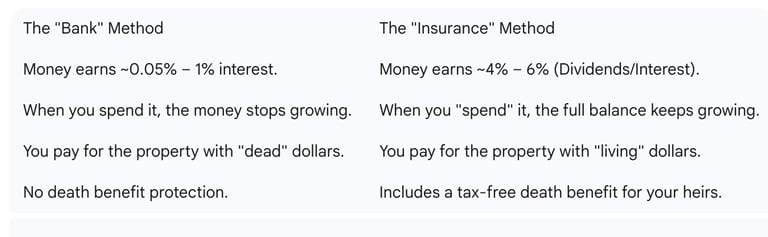

Avoiding Traditional Savings Pitfalls

Traditionally, individuals may consider saving for a down payment in standard savings accounts where the money tends to sit idle, yielding minimal interest. This conservative approach, while seemingly safe, often results in underutilization of capital. In contrast, utilizing a life insurance policy allows a person both protection and the option to access cash value, thereby enabling more strategic financial planning.

The 5-Step Blueprint:

Step 1: Build Your "Private Bank"

You start by over-funding a High Early Cash Value Life Insurance policy (usually Whole Life or IUL). Unlike a standard policy, this is structured so that 80%–90% of your premium is available as cash almost immediately.

Step 2: The "Policy Loan" Request

When you find a property, you don’t withdraw your money. Instead, you request a Policy Loan from the insurance company using your cash value as collateral.

The Big Idea: Your actual money never leaves the policy. It stays inside, continuing to earn dividends and compound interest on the full balance.

Step 3: Purchase the Property

You use the loan proceeds as your down payment.

Bank's Perspective: To the mortgage lender, this is often treated as "cash on hand."

Speed: There are no credit checks for a policy loan, and the funds are usually in your account within 3–5 business days.

Step 4: Use Rent to Pay Two People

Once your tenant moves in, the rental income covers your mortgage, taxes, and insurance. The "spread" (profit) is then used to pay back the insurance policy loan.

Flexibility: Unlike a bank loan, policy loans are often "unstructured." If you have a month with a repair or vacancy, you can choose to skip a loan payment to your policy without a penalty.

Step 5: Wash, Rinse, Repeat

Once the loan is paid back, your cash value is "restored." However, because your money stayed in the policy the whole time, it has been compounding for years. You now have a larger "bank" than when you started, ready to fund property #2.

Why This Beats a Regular Savings Account

A Quick "Math" Example

Imagine you have $100,000 in your policy.

You borrow $50,000 for a down payment.

The insurance company charges you 5% interest on that loan.

HOWEVER, the insurance company is still paying you a 5% dividend on the full $100,000.

Result: You are essentially borrowing money at a 0% net cost while your property appreciates in the real world..

In summary, the double play strategy provides a strategic financial pathway that merges life insurance and real estate investment. It turns traditional savings on its head, offering a dynamic method to create a robust wealth-building system that can be replicated repeatedly. With careful planning and execution, this strategy can yield significant financial freedom and security.

Get the Infinite Banking Ebook

Get updates on legacy and protection insights

© 2025 Kodgeti Group. All rights reserved.

Professional Disclaimer: Kodgeti Group provides strategic consulting and educational resources related to estate organization, legacy protection, and risk management. We are not a law firm, nor do we provide legal, tax, or specific investment advice. We strongly recommend that all final legal documents and insurance policies be reviewed by your personal attorney or licensed financial professional to ensure compliance with your local state laws.

Kodgeti Group: Real Estate & Wealth Protection

LINKS

EXPLORE THE KODGETI ECOSYSTEM

Newsletter